Death of A (Bio)Tech Bank

The Fall of Silicon Valley Bank

Last Friday, Silicon Valley Bank (SVB), the bank serving nearly half of US venture backed technology and life sciences companies, failed after experiencing the largest bank run in US history. The bank run appears to have been precipitated by fears of bank insolvency stroked by the announcement of an equity sale following large losses in SVB’s bond and mortgage-backed securities portfolio. Customers withdrew $42B, a quarter of the bank’s deposits, on Thursday triggering Federal Deposit Insurance Corporation (FDIC) intervention Friday morning. As of Sunday March 12th, SVB’s assets rest in an FDIC guided receivership awaiting liquidation or sale. However, in an effort to contain systemic risk, the Federal Reserve promised to fully protect depositors beyond the $250k FDIC insurance limit. Further, the Fed will enable access to funds on Monday morning averting a payroll crisis and possible bank-run cascade across regional banks.

Why is this relevant to the Biotech industry?

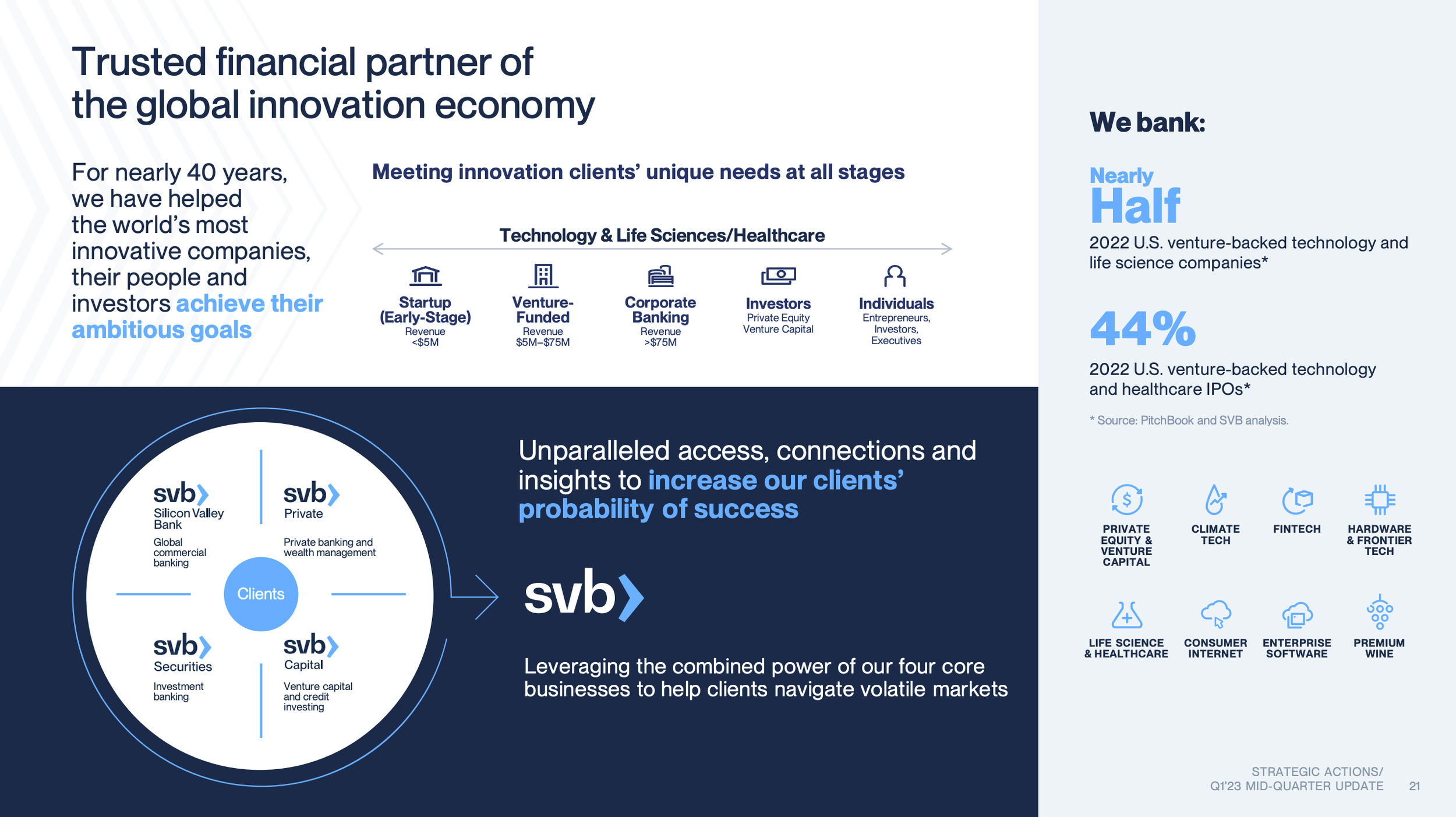

SVB was the go-to banking partner for early-stage and public biotechnology companies servicing over half of biotech start-ups and 44% of recently public biotechnology companies. SVB earned its market position by an unmatched suite of financial services to life sciences depositors. Notably, SVB could offer venture debt to its depositors that other banks wouldn’t or at rates better than competitors. Few other firms offer comparable services to early-stage biotech companies, and none at the scale of SVB.

SBV Corporate Presentation, March 8th (Slide 21)

In addition, SVB possessed an unparalleled degree of real-time market intelligence from its dominant position in the life sciences industry. While many investment banks service life sciences companies, few life-sciences investment banking franchises rivaled SVB Securities (née SVB Leerlink). In 2019 SVB Financial acquired the boutique biotech investment bank, Leerlink Partners to become a leading biotech financier. Loss of SVB Securities may disrupt financing of both publicly traded and privately held biotech companies. However, Bloomberg is reporting that Leerlink founder and SVB Securities head Jeff Leerlink may acquire the investment banking arm out of the bankruptcy.

Acutely, SVB’s collapse will disrupt financing activities. Without a sale of SVB, the structural impact of losing a key financial intermediary will be felt in the years to come. Successful drugs are a product of robust science, clinical execution, and a lot of money. Increased frictions in financing the development of new drugs will adversely impact the development of new drugs and the commercial deployment of biotechnology.

Loss of SVB’s institutional knowledge will open a niche for a new bank to claim. Perhaps the tech startup-focused banks like Mercury will fill the void. Finance runs on trust and confidence. SVB built trust and inspired confidence for decades. Loss of a trusted financial intermediary will create frictions that prevent investors building the conviction to take big risks. Building trust and confidence takes time. In the meantime, the future of medicine may have to wait.

What made SVB unique?

SVBs business model differed from traditional banks in two key ways. First, its customers were primarily investment funds and equity-financed businesses with little interest in traditional loan products. Therefore, SVB maintained large cash balances from its depositors, but made relatively few loans to its depositors [a]. Instead, SVB made money primarily by investing customer deposits in safe, interest-bearing assets, primarily liquid government-backed securities. This may seem like a small market, but when your customers routinely grow their bank balances by 10-100x, this commercial banking model can be lucrative.

Second, it exploited its market position and proprietary intelligence to build out complementary financial services products [b]. SVB specialized in lending against valuable, yet hard to value, assets. How much is an IP portfolio a biotech start-up worth as collateral? Or, a collection of premium wines of a 2017 vintage? Most banks would not lend against this collateral. However, SVB wasn't like most banks.

SVB maintained expertise to value these more exotic assets and provide liquidity to businesses that had few alternatives. While this sort of lending may be very risky for an average regional bank. Who would buy these assets in the event of a liquidation? Well, SVB as the dominant banking partner of life sciences startups, knew who might buy the collateral and at what price. In a tangible sense, these loans are less risky because SVB issued them!

Although this sort of debt might seem trivial, venture debt at 7-10% to bridge a company between financings can be the difference between survival and extinction. Few companies want to use this credit facility, but every company wants to have the option!

Lastly, many venture capital firms banked with SVB. Much like SVB offered complementary products to their startup clients, SVB built a business offering its VC clients lines of credit for general partner commitments, personal mortgages, and wealth management services [c].

Why did SVB Fail?

According to Silicon Valley lore, failure is usually overdetermined. But, we can at least outline the arguments we’ll hear over the next few weeks. For more detail, Matt Levine at Bloomberg has a great overview of SVB’s collapse. So does the NYTimes. And the Finanical Times. In a twist of cosmic irony, SVB’s seemingly high-risk lending didn’t precipitate the collapse. Rather, it appears the result of a bad bet on interest rates and the more mundane mechanics of banking. SVB paid too high a price for too many low-yield, low-risk assets exposing them to duration risk.

Taking a step back, a bank is an institution that borrows for short durations and lends for longer durations. A typical regional bank will take deposits from consumers, business, and high net worth individuals and lend these funds out to business and individuals in the form of short-duration credit lines and long-duration mortgages. Most banks make money by charging more for loans than they pay to depositors. For the bank, these loans are assets and deposits are liabilities.

As long as the value of the assets, and invested equity capital, are greater than the deposit liability, the bank is solvent. However, a bank is always to some degree illiquid; the long duration assets such as mortgages often can’t be sold immediately to pay a depositor [d]. But, the bank must maintain an appropriate liquidity ratio, in effect enough cash on hand to pay depositor requests. Now, the bank can become insolvent if the value of the assets declines by a value greater than the equity, or contributed capital, in the bank. If the bank is solvent, then it should be able to pay back all depositors following the sale of all its assets. If the bank is insolvent, then the bank cannot pay back all depositors even if all its assets were sold.

Cause #1: Insolvency Fears. SVB was insolvent at several points in Q4 2022 on a mark-to-market basis, as noted by Byrne Hobart and Ben Rubenstein.

How could this be? SVB had lots of deposits, more than 100% growth in deposits since 2019 after the venture financing boom of 2020-2021. For a bank, deposits are a liability. The customer can request funds at any point and the bank must meet that obligation. Most banks maintain a reserve, often at least 10% of outstanding deposits, and lend out the rest. But, SVB isn’t most banks.

Without many loans to issue, and with customers that often need a lot of money soon, SVB used most of its deposits to purchase low-risk interest-bearing securities - government bonds and mortgage backed securities. Through much of 2020-2021, the short-duration government bonds banks often hold as collateral were paying 0.25%. Instead, SVB purchased longer duration bonds and mortgage backed securities to achieve a better yield, 1.64% on average. In turn, the bank locked away cash for nearly a decade at historically low yields. By the end of 2022, short-term government debt traded at a 5% yield.

Yield on the 1-year Treasury Bill (2010-2023) via Macrotrends.net

As the value of a bond is inversely related to the interest rate, the value of SVB’s securities portfolio took a big hit - $15.1B. This loss was on par with the $16.3B in total equity of the bank putting SVB on the brink of insolvency. But, this had been the case for a while. Marc Rubinstein noted that:

“So big was this drawdown that on a marked-to-market basis, Silicon Valley Bank was technically insolvent at the end of September. Its $15.9 billion of HTM mark-to-market losses completely subsumed the $11.8 billion of tangible common equity that supported the bank’s balance sheet.”

How was this possible? Well, bank accounting rules classify securities as Held-to-Maturity (HTM) or Available-for-Sale (AFS). HTM securities are valued at cost, assuming that the bank will hold the security and receive all payments. In contrast, AFS securities are valued mark-to-market, or based on what someone would pay for them. If rates rise, the value of the bond declines, but the nominal value does not change. Therefore, HTM securities can see large changes in their mark-to-market value but banks do not need to change the value on their books as they plan to hold to maturity. Ben Rubeinstein again: “So how could the bank have satisfied customers’ deposit demands? One thing it couldn’t do is tap into its held-to-maturity securities portfolio. The sale of a single bond would trigger the whole portfolio being market to market which the bank didn’t have the capital to absorb.” Therefore, if depositors needed more money faster than expected, SVB would need to sell its HTM portfolio and revalue it. With rising interest rates, many banks will have to realize similar losses.

Cause #2: Signals of Financial Weakness. As noted above, SVB was insolvent from time to time over nearly six months before imploding. But, rather inexplicably in my estimation, nobody really cared? On February 23rd, Byrne Hobart pointed out that a mark-to-market valuation of SVB’s securities had the bank levered 185:1.

No bank wants to be in this position. If depositors demand more money, then forced selling of the securities to meet demands could trigger a solvency crisis. But, one would need a massive bank run to happen to force the sale of enough securities to force the bank to realize losses on their HTM securities portfolio. Unfortunately, two weeks later, SVB got hit by the largest single-day bank run in US history.

Accelerating the fears were the actions the bank took to acknowledge the losses in their securities portfolio and raise new capital. Sometimes, admitting it is the first step. For SVB, admission was the first step to collapse! Realizing losses and taking action to improve the financial position of the bank may have stoked insolvency fears and helped drive the bank run.

Cause #3: Prisoner’s Dilemma. In game theory, a prisoner’s dilemma is a situation where two parties must either cooperate for mutual benefit or defect for personal gain. During a bank run, if you manage to withdraw your money before everyone else, you get to keep your cash. Withdrawal accelerates the bank run. However, if everyone independently chooses not to withdraw, the bank continues to exist.

So, if you expect the bank to experience a run, a rational independent actor would withdraw funds. Once word of a bank run starts spreading, it becomes difficult to halt a bank run. The payoff to withdraw is asymmetric: remain and maybe lose some money, or withdraw and avoid loss. For an advisor with a fiduciary duty, such as a board member, it’s hard to argue against withdrawal if a bank run has started. So, you and all your advisees defect and the bank goes under! Belief of a possible bank run has precipitated a bank run! In the past, transactional frictions have given bank regulators time to intervene and avoid smaller liquidity crises.

Cause #4: Social Media and Frictionless Banking. In the past, word of a bank run would be spread over the course of several days from neighbor to neighbor, or via large broadcast media at worst. Now, rumors of a bank run are available at the tap of a screen. Is it too easy for algorithmically curated feeds of too-online investor-influencers to create the appearance of a bank run, which could precipitate an actual bank run? Perhaps. But, in the era of physical banking, you’d have lines to wait in to withdraw. Now? Just a few more taps on the same phone in your preferred bank app and your money is now safe! Why take the risk by keeping your money in the bank? Frictionless banking coupled with a prisoner’s dilemma seems like a lethal combination. I’m not sure one can argue this combination caused a bank run. But, it certainly didn’t slow it!

Cause #5: S. 2155. Trump signed the “Economic Growth, Regulatory Relief, and Consumer Protection Act” in 2019 increasing the threshold for bank stress-testing from $50B to $250B in assets. SVB would have been at the edge of this threshold. Multiple politicians have cited this as a Dodd-Frank provision that would have prevented the crisis. I disagree. First, as pointed out by Jing Liang, the stress tests the Fed runs has scenarios that appear too narrow. “Severely Adverse” conditions represent a 1% increase in the yield of the 10 year T-bill. In the past year, the 10 year T-bill yield is up from 2% to 3.7%. The 1-year T-bill rose from 1% to 5.2% in a year. It seems likely SVB would have passed any stress test. Second, the insolvency and liquidity crises are the result of using valuation methods for HTM securities that don’t reflect their valuation in a crisis. S. 2155 didn’t fix this. Crises often violate assumptions of valuation, in this case the hold portion of hold-to-maturity.

Outlook

Unless the Fed manages to find a buyer of SVB, which appears unlikely given the guarantees promised to depositors, the biotech ecosystem has a big hole to fill. Biotech is a risky, capital intensive industry. Financial intermediaries help bring liquidity to the financing market. Loss of a key, locally-important financial intermediary like SVB will disrupt capital flows preventing drugs from making it into the clinic.

Could the demise of SVB been averted by a capital raise preceding the announcements of losses? Perhaps. But, it’s hard to raise capital with losses looming. Perhaps the PR fanned the flames of fear. Hopefully we won’t replay this episode next month to find out.

As the Financial Times points out, “[SVB] committed a cardinal sin in finance. It absorbed enormous risk with only a modest potential pay-off in order to bolster short-term profits” 10. It’s hard to argue that the duration risk of SVB’s securities portfolio was worth the extra fraction of a percentage point in yield. For SVBs risk sins, patients will pay.

The imminent crisis has been averted, for now. SVB wasn’t the only bank with major duration risk. The Fed has stemmed the problem for now, but there are many outstanding losses for banks to absorb absent cash injections. The Fed finds itself in a tight spot trying to limit excess reserves to control inflation whilst banks need additional capital to absorb impending losses.

Footnotes

[a] In contrast, most regional banks make their money issuing loans to their existing depositors. In theory, through depository and personal relationships, they have better information about the creditworthiness of their depositors and can better price the risk of a given loan than a large, systemically important bank (e.g. JPMorgan, Wells Fargo).

[b] To maintain banking relationships, SVB also offered key customers low-interest loans against illiquid company stock and prime-rate mortgages.

[c] SVB also provided wealth management services to its high net worth clients. As one might expect, VCs liked the complementary services.

[d] In contrast, a brokerage or cryptocurrency exchange should always be both fully liquid and fully solvent because they are custodians for their customers. If all customers ran to withdrawal securities and cash from a brokerage, the brokerage should be able to meet these demands within a couple days. If your brokerage/cryptocurrency exchange can’t meet this standard, you’re using a shadow bank or ponzi scheme.